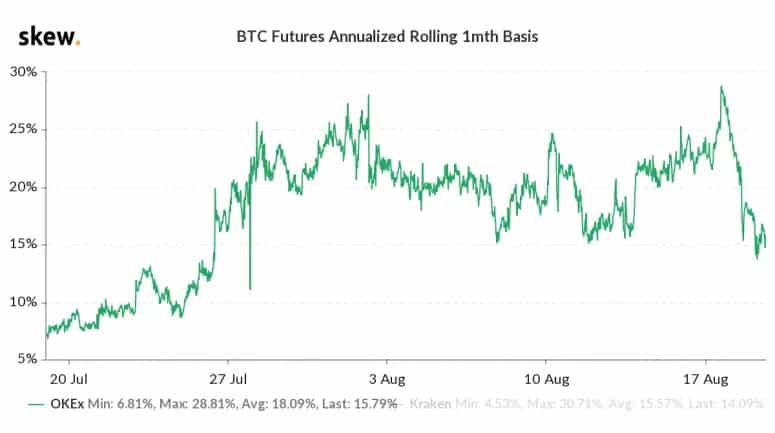

Formal demand for stablecoins may decrease because the yield on ‘carry trades’ has halved since this Monday. The annualized rolling one-month futures basis went as high as 28 percent at the beginning of the week on the Malta-based crypto exchange OKEx, the largest one when it comes to open interest.

That was the greatest premium since February, as per data offered by the crypto derivatives research company Skew. That premium, though, went down by 14 percent in under 48 hours. Simply put, the carry strategy, if started now and held until Friday, will yield an annualized return of 14 percent down from 28 percent on Monday.

Cash and Carry Strategy

Carry trading, or cash and carry arbitrage, is a market-unbiased strategy, one that looks for profit from both increasing and decreasing prices in one or multiple markets. It implies purchasing the asset in the spot market and, at the same time, selling a futures contract against it when the futures contract is trading at a premium to the spot price.

The premium, though, disappears as the futures contract is close to expiration, and on the day of the settlement, the futures price rallies with the spot price. If futures draw high premium, savvy traders start a carry strategy and lock in fixed returns.

Futures markets normally trade at a premium to the spot market, and the expansion tends to widen during price rallies. The annualized premium grew, with approximation, from 9 percent to 27 percent in the last two weeks of July as Bitcoin’s price increased from $9,000 to $12,000 and stayed close to that level heading into August.

Traders had the possibility to lock in an annualized profit of 28 percent on Monday by purchasing Bitcoin in the spot market and selling the front-month futures contract on OKEx. Carrying out that trade now would still gain profit, but only by half as much.

The Carry Trades Seem to Have Cooled Off

The cool of the carry strategy yield could also lead to a reduction in demand for dollar-backed stablecoins such as Tether (UDST).

“Stablecoins are widely used as funding currencies, and there has been a high demand for these dollar-backed cryptocurrencies from institutions,” Skew CEO Emmanuel Goh said. Indeed, the carry trade has been one of the main reasons for the surge in stablecoin issuance seen this year.

On Monday, the annualized cost of borrowing Tether on the decentralized finance protocol Compound was 6.94 percent. Presuming that carry traders borrowed UDST from Compound on Monday, keeping the carry strategy until the August expiry, which is due next Friday, would produce a net yield of around 21 percent in annualized terms.

If this strategy were carried out now by borrowing USDT, the net yield would be 6.3 percent. The reason for this is the fact that the cost of borrowing USDT is now 7.68 percent and the OKEx futures are trading at a premium of 14 percent. In other words, carry trades have become less appealing, and therefore, institutional demand for stablecoins could cool off, as noted by Skew.

The premium has reduced a lot in the last 48 hours, probably because of Bitcoin’s failed attempt to break the $12,000 line and resulting in concern of deeper price retreats. The decline in premium may have been mixed by boosted selling in futures as more traders stacked into the cash and carry trade.